Small Language Models in Insurance 2026: Why Carriers Are Moving Beyond Frontier LLMs

Frontier LLMs got insurance into the AI game. In 2026, small language models are quietly winning the production race. Here is the complete guide to how SLMs are reshaping underwriting, claims, fraud detection and compliance — at a fraction of the cost and with the governance regulators actually want.

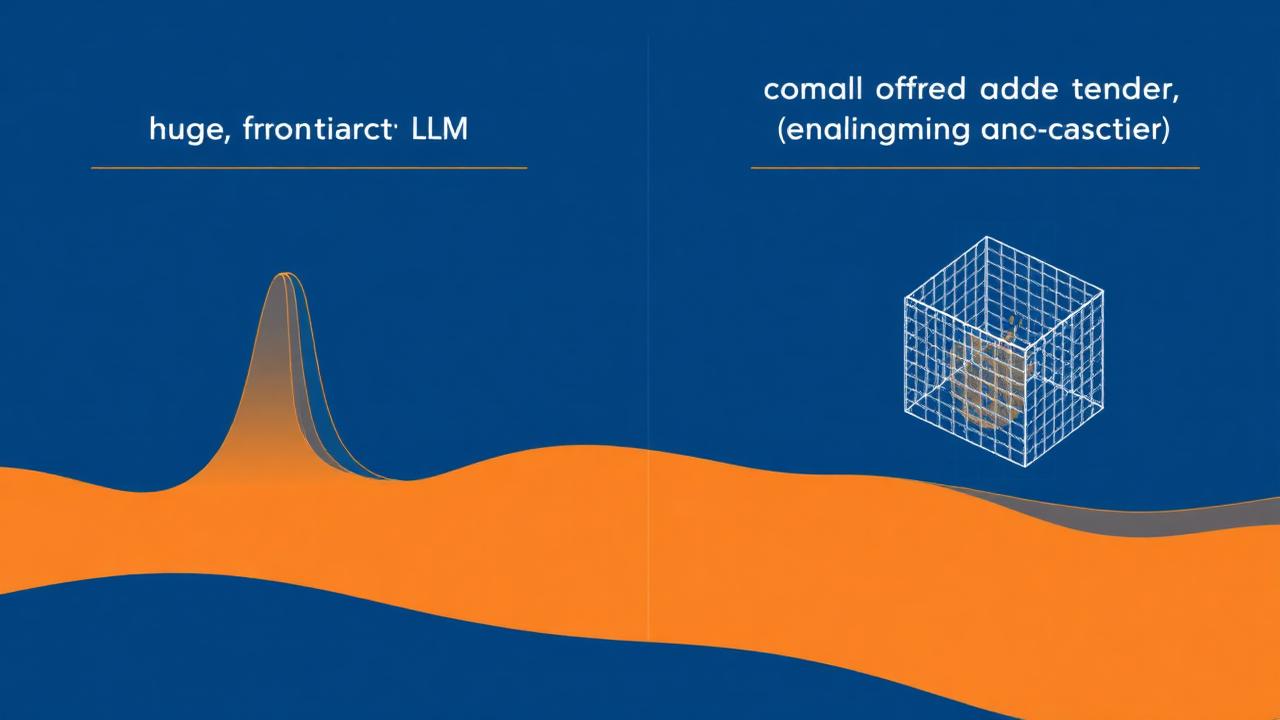

For the last three years, the story of AI in insurance has been the story of frontier large language models. Carriers signed enterprise deals with the biggest model providers, plugged GPT-class systems into claims and underwriting pilots, and watched their cloud bills climb. The pilots worked — sort of. They proved the value. They also proved the cost, the latency and the governance headaches. In 2026, a quieter shift is happening inside the industry's AI stack: carriers are moving production workloads off frontier LLMs and onto small language models — compact, fine-tuned, often on-premise systems that are cheaper, faster and far easier to govern. This is the complete 2026 guide to small language models in insurance: what they are, why they are exploding now, where they outperform their giant cousins, and what carriers, MGAs and InsurTechs need to do to stay ahead.

What a small language model actually is

A small language model — or SLM — is a generative AI model with a parameter count typically in the range of one to fifteen billion, compared to the hundreds of billions or trillions in frontier LLMs. The label is a little misleading. "Small" here means "compact relative to GPT-class systems," not "weak." Modern SLMs like the Phi, Gemma, Mistral and Llama 3 families can match or exceed much larger models on narrow tasks once fine-tuned on domain data.

In an insurance context, that distinction matters enormously. Carriers do not need a model that can write poetry, debate philosophy and code a video game. They need a model that can read a loss run, summarize a policy, extract clauses from a submission, and answer questions about a rating manual — accurately, repeatedly, and within strict regulatory boundaries. That is exactly the kind of task profile SLMs were built for.

Frontier LLMs vs small language models, at a glance

- Cost: SLMs are often 10–50x cheaper per token than frontier LLMs at comparable accuracy on narrow tasks.

- Latency: SLMs respond in tens of milliseconds; frontier LLMs typically need hundreds.

- Deployment: SLMs can run on-premise, in a private cloud or even on a laptop — frontier models almost always require external API calls.

- Governance: SLMs make data residency, audit logging and PII control dramatically simpler.

- Customization: SLMs can be fine-tuned on a carrier's own data without leaking IP to a model provider.

Why 2026 is the breakout year for SLMs in insurance

Three forces are converging in 2026 to push SLMs from research curiosity to production default. The first is regulatory clarity. The EU AI Act, the NAIC Model AI Bulletin and a wave of US state guidance have made one thing clear: insurers are accountable for every AI output that touches a policyholder. That accountability is much easier to demonstrate with a model the carrier actually owns and can audit, line by line.

The second force is economics. As GenAI moved from pilot to scale, finance teams started asking uncomfortable questions about per-claim and per-quote AI costs. A frontier LLM that costs pennies per call sounds cheap until you multiply it by ten million claims a year. SLMs collapse that cost by an order of magnitude while delivering equal or better quality on the narrow tasks that dominate insurance workflows.

The third force is technical maturity. Open-weight SLMs released in 2024 and 2025 closed most of the quality gap with frontier models on enterprise tasks. Tooling for fine-tuning, evaluation and retrieval-augmented generation matured. And inference infrastructure — from NVIDIA's enterprise stack to AWS Bedrock and Azure AI Foundry — finally made it straightforward to deploy and monitor a fleet of SLMs in production.

Where SLMs are winning in insurance today

The highest-value SLM use cases in 2026 share three traits: they are high-volume, narrowly scoped, and sensitive to cost, latency or data residency. That covers a surprising amount of the insurance value chain.

1. Underwriting document intake

Submissions are a torrent of unstructured text — ACORD forms, loss runs, SOVs, brokers' emails, prior policies. SLMs fine-tuned on a carrier's own underwriting corpus can extract structured data from this torrent at a fraction of the cost of a frontier LLM, with response times fast enough to embed directly inside the underwriter's workbench. McKinsey's research on AI in insurance has highlighted submission intake as one of the highest-ROI productivity opportunities in commercial lines.

2. Claims summarization and triage

Claims files are long, repetitive and full of jargon — exactly the kind of text SLMs handle well after fine-tuning. Carriers are using SLMs to generate first-notice-of-loss summaries, draft adjuster notes, and triage incoming claims by complexity. Because the model runs in the carrier's own environment, sensitive medical and financial details never leave the perimeter.

3. Fraud detection support

Fraud teams need models that can read claim narratives, social posts and adjuster notes for subtle linguistic red flags. SLMs fine-tuned on historical fraud cases catch patterns frontier models miss, and they do it without sending sensitive investigation data to a third-party API.

4. Agent and broker copilots

The front-office copilots reshaping distribution in 2026 increasingly run on a hybrid stack: a frontier LLM for complex reasoning and an SLM for the high-frequency drafting, summarization and lookup tasks that dominate day-to-day producer work. The result is a copilot that feels instant and costs a fraction of an all-frontier setup. We covered the productivity side of this shift in our guide to AI copilots for insurance agents in 2026.

5. Compliance, audit and regulatory reporting

Drafting Form 10-K disclosures, summarizing market-conduct exam findings, reconciling state filings — none of this needs a trillion-parameter model. SLMs handle it cheaper, faster, and inside the compliance perimeter where regulators want it.

The architecture: how carriers are actually deploying SLMs

The pattern emerging across leading carriers in 2026 is not "SLMs instead of LLMs." It is a tiered model stack, with the right model at the right layer.

- Tier 1 — Edge SLMs (1–3B parameters): embedded in agent desktops and mobile claims apps for instant drafting, summarization and form-filling.

- Tier 2 — Domain SLMs (7–15B parameters): fine-tuned on the carrier's policy library, underwriting guidelines and historical claims, running in a private cloud for core workflows.

- Tier 3 — Frontier LLMs: reserved for complex reasoning, multi-document synthesis and rare edge cases — called sparingly through governed APIs.

- An orchestration layer that routes each task to the cheapest model that can handle it within accuracy and latency targets.

This tiered approach is what allows carriers to scale GenAI to millions of transactions without scaling the cost in lockstep. It is also a natural fit for agentic systems — the same multi-agent patterns we explored in our analysis of agentic AI in insurance claims — because cheap, fast SLMs make multi-step agent workflows economical.

Governance, compliance and the regulator's view

Regulators are not neutral on the SLM shift. They quietly prefer it. A model the carrier owns, can audit, can patch and can host inside its own data perimeter is far easier to supervise than a black-box external API. That alignment with regulatory expectations is one of the underrated reasons SLMs are accelerating in 2026.

The governance checklist for SLM deployments

- Document training and fine-tuning data lineage end to end.

- Run pre-deployment bias and fairness evaluations on insurance-specific test sets.

- Maintain immutable audit logs of prompts, retrievals and outputs.

- Implement PII redaction and data-residency controls aligned with EU and state rules.

- Set monitoring thresholds for drift, hallucination and accuracy degradation.

- Disclose AI use to consumers where the EU AI Act or state law requires it.

- Keep a human in the loop for any decision affecting coverage, pricing or claims outcomes.

What SLMs do not replace — and the limits to know

SLMs are not a silver bullet. They underperform frontier LLMs on open-ended reasoning, long-context synthesis across many documents, and creative tasks. They also require real investment in data curation, evaluation harnesses and MLOps — the cost moves from the API line to the engineering line. Carriers that try to skip the fine-tuning and evaluation work end up with cheap models that quietly produce expensive errors.

- Avoid SLMs for tasks that need broad world knowledge or multi-step open-ended reasoning.

- Do not deploy without an insurance-specific evaluation harness — generic benchmarks lie.

- Plan for re-tuning as products, regulations and risk appetite change.

- Budget for inference infrastructure and observability, not just model training.

How to start an SLM program in 2026: a 90-day playbook

Carriers that have moved fastest in 2026 share a common playbook. It is unglamorous, sequential, and disciplined.

- Days 1–15: Pick two narrow, high-volume workflows where you already run a frontier LLM in production.

- Days 16–30: Stand up an SLM baseline (open-weight, no fine-tuning) and benchmark it head-to-head against the frontier model.

- Days 31–60: Fine-tune the SLM on a curated slice of your own data; build the evaluation harness; close the accuracy gap.

- Days 61–90: Shadow-run the SLM in production, measure cost, latency and edit rates, then progressively shift traffic.

- Day 90+: Add the SLM to your tiered routing layer, expand to the next workflow, and lock down governance and monitoring.

What comes next: domain foundation models for insurance

The next chapter, already in early development at several reinsurers and InsurTech consortia, is the insurance-specific foundation model — an SLM-scale model pre-trained on a vast corpus of policy wordings, claims, actuarial reports and regulatory filings. Combined with parametric and embedded distribution models, these domain-native systems will be the substrate of the next decade of insurance AI. We will track that shift in our broader coverage of the future of insurance AI.

The bottom line for insurance leaders in 2026

Frontier LLMs proved the case for AI in insurance. Small language models are turning that case into a sustainable business. The carriers, MGAs and InsurTechs that win the next phase will not be the ones with the biggest model. They will be the ones with the right model, in the right place, governed the right way — and a stack disciplined enough to know the difference. SLMs are not the end of the frontier era. They are how insurance finally industrialises AI.

Related reading on InsurAI Buzz

If you found this guide useful, you may also want to read our deep dive on AI copilots for insurance agents in 2026, our analysis of agentic AI in insurance claims, our guide to AI cyber insurance pricing, and our outlook on the future of insurance AI.

Sources and further reading

Key takeaways

- Small language models are the breakout 2026 trend in production AI insurance stacks.

- SLMs are 10–50x cheaper than frontier LLMs on narrow insurance tasks at equal or better accuracy.

- The winning architecture is tiered: edge SLMs, domain SLMs and frontier LLMs orchestrated together.

- Governance, audit and data residency are dramatically easier when carriers own and host the model.

- Insurers without an SLM strategy in 2026 will struggle to scale GenAI economically into 2027.

Continue learning on InsurAI Buzz

- AI Voice Agents in Insurance 2026: How Conversational AI Is Rebuilding the Contact Center — Insurance Chatbots

- AI Copilots for Insurance Agents in 2026: How Generative AI Is Rebuilding the Front Office — AI Automation

- Parametric Insurance and AI in 2026: How Instant Payouts Are Reshaping Climate and Catastrophe Coverage — Future of Insurance AI

Frequently asked questions

What is a small language model in insurance?

A small language model (SLM) in insurance is a compact generative AI model — typically 1 to 15 billion parameters — fine-tuned on a carrier's own policies, claims and underwriting data. SLMs handle narrow insurance tasks like document intake, claims summarization and compliance drafting at a fraction of the cost and latency of frontier LLMs, while running inside the carrier's own data perimeter.

Why are insurers moving from frontier LLMs to SLMs in 2026?

Three forces are driving the shift: regulatory clarity from the EU AI Act and NAIC Model Bulletin, the economic reality that frontier LLM costs do not scale to millions of claims and quotes, and the technical maturity of open-weight SLMs that now match frontier models on narrow insurance tasks.

Where do small language models outperform large LLMs in insurance?

SLMs outperform on high-volume, narrowly scoped, latency-sensitive tasks: underwriting document intake, claims summarization, fraud-language detection, agent copilots and regulatory drafting. Frontier LLMs still win on open-ended reasoning and complex multi-document synthesis, which is why most 2026 architectures combine both in a tiered stack.

How should an insurer start a small language model program?

Start with two narrow, high-volume workflows already running on a frontier LLM. Benchmark an open-weight SLM baseline, fine-tune on curated internal data, build an insurance-specific evaluation harness, then shadow-run in production for 60–90 days before shifting traffic. Pair the rollout with audit logging, PII controls and human-in-the-loop review.

Stay ahead of AI in insurance

Subscribe for weekly analysis trusted by underwriters, claims leaders and insurtech founders.

Subscribe freeRelated reading

Best AI Tools and Software for Insurance Teams in 2026

We compared the leading AI platforms across underwriting, claims, fraud and customer service. Here is what we recommend.